Raj Singh Thakur

KF Rookie

Low risk , not complicated, genuine advice, genuine source, duration of less then 1 year to 2 year.

Liquid fund / FD in an SFB / Conservative hybrid fundLow risk , not complicated, genuine advice, genuine source, duration of less then 1 year to 2 year.

You can distribute your fund in 2 liquid funds or in liquid fund and FD.Low risk , not complicated, genuine advice, genuine source, duration of less then 1 year to 2 year.

Hi @Raj Singh ThakurLow risk , not complicated, genuine advice, genuine source, duration of less then 1 year to 2 year.

Hie Mr Shavir,Hey @Prince , curious to know - how can you earn 14% from T-Bills?

")

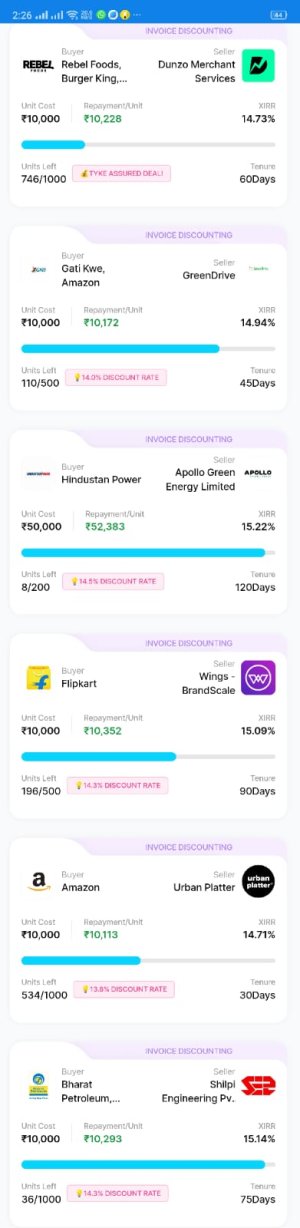

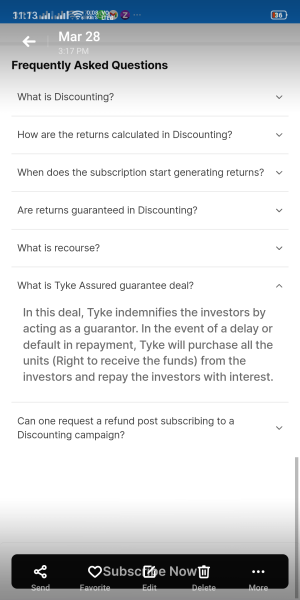

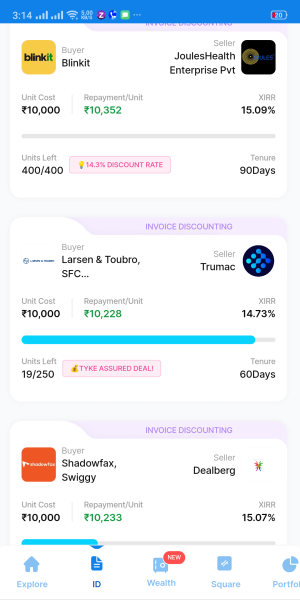

Yes it's risky, there is an risk mitigation also, time in time tyke issue invoice on which they assured the deal and provide guarantee also. Enclosed the snap of deal recently closed in March last week.No worries @Prince , just to add a small disclaimer

Invoice Discounting is a risky investment (probably more than Stock Market), and investors must take caution before investing their hard earned money

Low risk , not complicated, genuine advice, genuine source, duration of less then 1 year to 2 year 4 to 6 lakh for a one-year duration with a desire for high returns at low risk is a challenging proposition, as high returns often come with higher levels of risk. However, there are some relatively low-risk options you could consider:

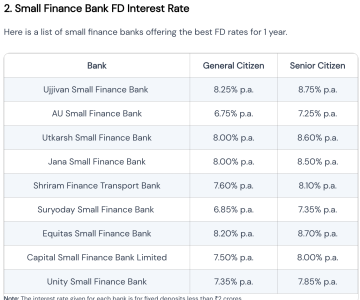

GO THROUGH FD IN STABLE MONEY APP.Low risk , not complicated, genuine advice, genuine source, duration of less then 1 year to 2 year.